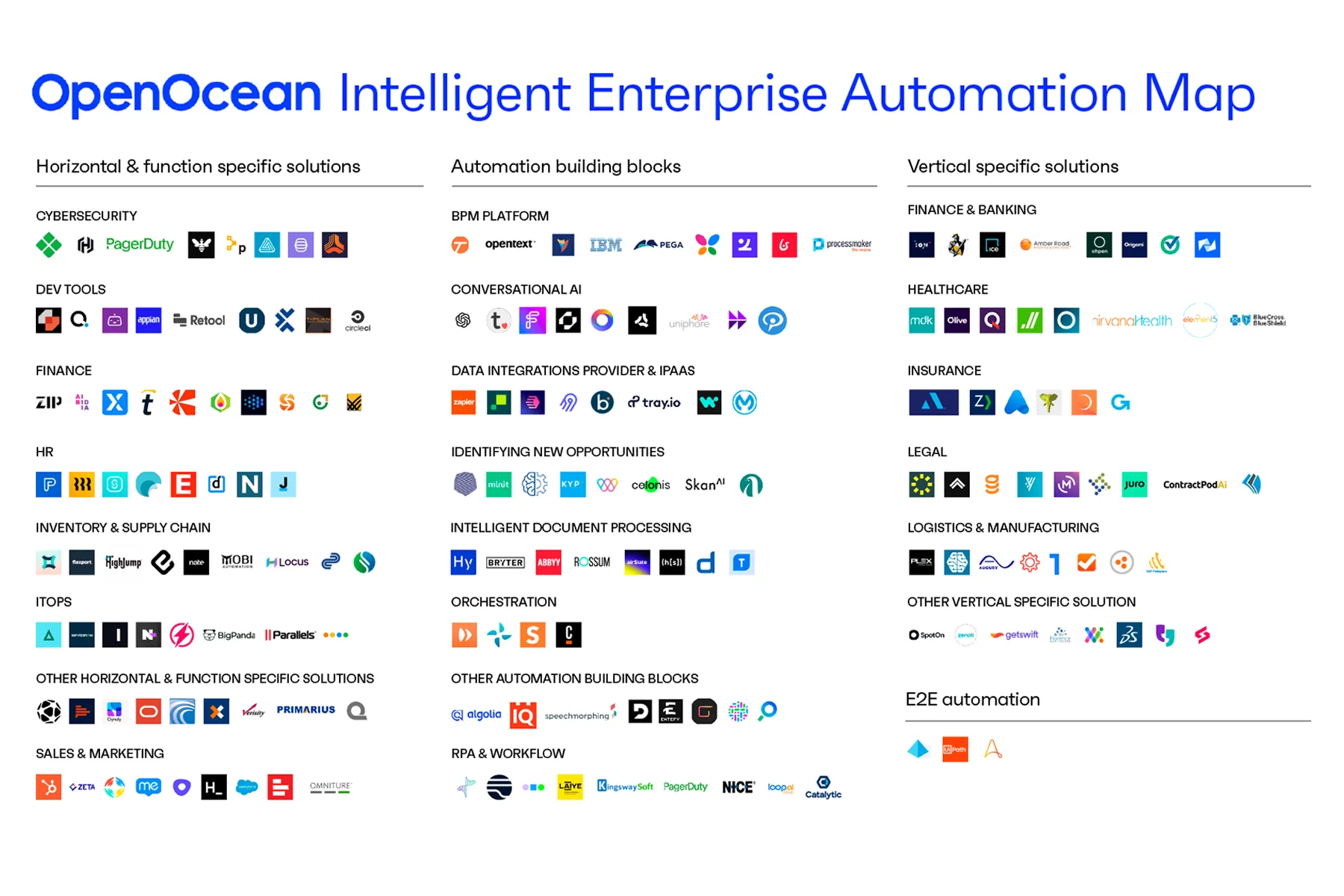

OpenOcean's automation database provides a comprehensive view of the expansive landscape of enterprise automation software. For our 2023 market map we have meticulously curated a collection of over 810 automation companies, marking an increase of approximately 100 companies from the previous year. The market map is designed to capture the leading enterprise automation software companies in the world with estimated valuations exceeding $100M, along with the most promising early-stage startups in this domain aiming to revolutionise enterprise operations.

“Enterprise automation remains one of the largest and most exciting areas for software startups over the long term. The recent explosive growth of AI innovation only accelerates the path to truly intelligent and holistic automation, the holy grail of operating enterprises at the next level with the help of technology”, explains Tom Henriksson, General Partner at OpenOcean.

Key highlights of the 2023 Automation Market Map:

- This year’s database includes 811 companies, marking a ~15% increase from last year

- Private capital investments in enterprise automation companies exceeded $11Bn in 2022, and this number has already been exceeded in just H1/2023

- 13 new unicorns emerged

- LLMs and generative AI are expected to reshape the enterprise automation space in the years to come

Explore the 2023 Automation Market Map here.

The Enterprise Automation Domain Continues to Attract Investments Despite a Slower Market Environment

In 2022, enterprise automation software companies experienced a decline in private funding compared to the record-high levels seen in 2021. Over the course of the year, private investors invested a total of ~$11.3Bn into automation companies, marking a drop of approximately 33% from the previous year. This decline can be attributed primarily to a decrease in capital raised through IPOs, which amounted to only ~$1Bn in 2022 compared to ~$4.5Bn in 2021, and a more than 50% reduction in PE/growth stage financing in general.

Despite the challenges, enterprise automation companies attracted more funding compared to the overall market, which experienced an approximate 45% decrease in invested private capital between 2021 and 2022. The first half of 2023 has already surpassed the invested capital in 2022 and ended the H1 with ~$13,5Bn invested into enterprise automation companies. The major driving force behind the surge was OpenAI's remarkable $10.3 billion investment round led by Microsoft. Looking ahead, we anticipate the fundraising activity to gradually pick up during the second half of 2023. Additionally, we expect to witness the emergence of substantial early-stage deals.

Later-stage VCs were again leading the way in 2022, investing a total of ~$9Bn into enterprise automation companies. Early-stage VC grabbed the second spot, investing a total of ~$1.2Bn into the domain. Capital raised via an IPO was drastically cut to only ~$1Bn in 2022, following the general IPO trend of 2022, with Nasdaq not seeing a single IPO valued in excess of $1Bn. Nevertheless, even with the slow IPO market, an impressive 13 new unicorns emerged, bringing the total count of enterprise automation companies valued at over $1Bn to 92 in the automation map (four unicorns omitted due to removal of two categories “Self driving vehicles” and “Telecom”).

Even though 2022 did not break any investments record, notable highlights from the year include;

- Flexport’s Series E of $935M, which stood out as the largest single funding round.

- A monumental investment by Microsoft, leading OpenAI's staggering $10.3Bn investment round. OpenAI's massive round was followed by Rippling, the employee management platform, with a $500M series E round. As a result, the total capital invested in automation companies during the first half of 2023 has already surpassed that of the entire 2022.

- A total of 28 companies raised over $100M in 2022, two thirds of the 44 companies doing so in 2021.

- Within the first six months of 2023, five companies have raised over $100M.

The United States maintained its dominant position in the enterprise automation market, with approximately 60% of companies having their headquarters there, although this was a slight decrease from the ~70% observed in 2021. Europe remained in the second position, hosting ~22% of all automation companies, marking a slight increase from 2021.

Notably, the ITOps segment, including companies like ServiceNow, emerged as the highest valued segment, boasting an impressive average company valuation of approximately ~4Bn. Followed by the E2E automation segment, which includes UiPath, and the Sales & Marketing segment, which encompasses industry giants like Salesforce and startup leaders like OpenOcean’s portfolio company Supermetrics.

Despite challenging market conditions, enterprise automation companies showcased remarkable resilience, drawing continued interest and investment from venture capitalists. This signals a promising outlook for the industry in the coming years, a sentiment echoed by Gartner’s projection that the market for hyper-automation will reach over $1 trillion by 2026.

Generative AI Sparks Automation Revolution in Enterprise Space

During the research phase, numerous startups and scaleups within the enterprise automation space had already begun implementing or discussing the implementation of Large Language Models (LLMs) into their current product suites. The adoption of LLMs and generative AI among existing players is expected to continue throughout the year, thanks to the growing accessibility of models from OpenAI, Meta’s Llama, Stanford’s Alpaca, and many others readily available.

This year’s automation market map has yet to fully depict the implications of LLMs and generative AI and how they will reshape the enterprise automation space. We anticipate the emergence of disruptive players in the coming years, further enhancing the automation possibilities across all categories within the broader enterprise automation domain. For instance, in a few years we expect to see fully functional workflow automations designed and executed using LLMs. Moreover, we expect new categories to arise, enabled by customisable large language models. Notably, DevTools are at the forefront of this transformative movement, and countless entrepreneurs are working on enterprise-wide search and automation tools harnessing the power of LLMs. As the LLM landscape is rapidly developing we have yet to include a separate category for LLMs, even though numerous companies could be categorised within it.

The technical advances in the generative AI space are happening at an incredibly rapid pace, achieving in weeks what one could have expected to take years. In some cases, the time in which generative AI is estimated to achieve human-level performance is 40 years sooner than experts previously thought (McKinsey & Co.). Just a decade ago no AI system could accurately provide language or image recognition at a human level, whereas now, machines can even outperform humans in language and image recognition in some tests (Giattino et al. 2023). As the space is maturing both in terms of capabilities and solutions supporting their adoption, generative AI are starting to reach performance levels making them usable in real-world use cases and adoption is picking up. This will generate significant growth in enterprise automation.

“As the enterprise automation space evolves, we can expect to witness a surge in groundbreaking applications that were previously unimaginable. From revolutionising customer interactions to streamlining internal processes with automated content creation and data analysis, LLMs have the potential to redefine the way businesses operate. With the emergence of market-disruptive players, the competitive landscape is bound to change rapidly. Companies that successfully adopt and integrate LLMs into their product offerings are likely to gain a significant advantage. Simultaneously, new entrants that bring innovative ideas and customised AI solutions will challenge existing enterprise automation players”, concludes Crystal van Oosterom, AI Venture Partner at OpenOcean.